BRIEFING

Key SFC Licensing Issues for Virtual Asset Managers, Virtual Asset Funds Distributors and Virtual Asset Trading Platform Operators

Download PDF————————————————————————————————-

BACKGROUND

On 1 November 2018, the Hong Kong Securities and Futures Commission (the “SFC”) issued a number of announcements that would potentially have a regulatory impact on those who conduct financial activities involving virtual assets in Hong Kong. These announcements include a “Statement on regulatory framework for virtual asset portfolios managers, fund distributors and trading platform operators”[1] (the “Statement”) and “Circular to intermediaries – Distribution of virtual asset funds” [2] ((the “Circular”) which, together with the Statement, are referred to as the “SFC Announcements”). The SFC Announcements have created hype and fear (and perhaps myths) in equal measures. Given these reactions, it is important to bear in mind at the outset that the SFC Announcements did not introduce or announce any new laws. The SFC Announcements proposed new regulatory measures that are all within the “regulatory remit” of the SFC and are primarily aimed at enhancing investor protection. The impact which the SFC Announcements may have on virtual asset managers, virtual asset funds distributors and virtual asset trading platform operators varies depending on what role each plays in relation to virtual assets, whether it is an existing SFC licensed corporation and what type of virtual assets is involved (most importantly, whether the virtual assets that are involved are considered to be “securities” or “futures contracts” – those that are considered to be securities or futures contracts will be referred to as “SF Virtual Assets” and those that are not considered to be either “securities” or “futures contracts” will be referred to as “non-SF Virtual Assets” for the purpose of this article). Although the SFC Announcements contain important clarifications on some previously uncertain issues, significant uncertainties still remain (and new uncertainties may have emerged). In particular, there are no clarifications as to what type of virtual assets amount to “securities” or “futures contracts” and what type of virtual assets do not. However, the fact that the SFC Announcements did acknowledge that some virtual assets may amount to “securities” or “futures contracts” whilst some may not, may in itself be significant.

REGULATORY IMPACT ON VIRTUAL ASSET MANAGERS AND VIRTUAL ASSET FUNDS DISTRIBUTORS

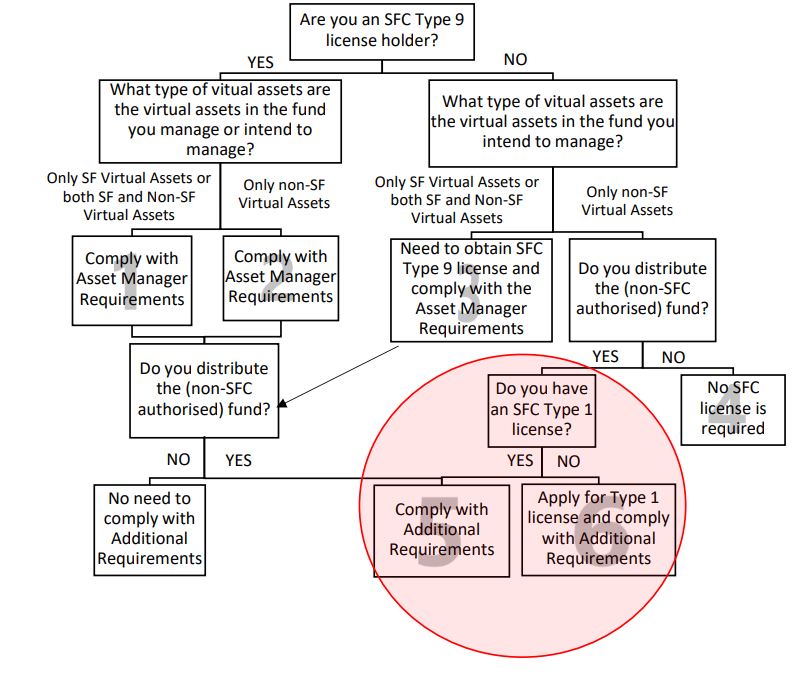

The diagram below captures how virtual asset managers and/or virtual assets fund distributors (the section highlighted in red) will be subject to new regulatory and licensing requirements following the SFC Announcements and the consequences that follow are as explained below. To varying degrees, the SFC Announcements would have a regulatory impact if a market participant falls within any one of the Boxes except for Box 4. However, as noted above, the key question in the overall licensing and regulatory roadmap remains whether the virtual assets involved are considered to be “securities” or “futures contracts” or neither. The SFC Announcements do not contain any further clarification as to where the line may be drawn between those virtual assets which are to be considered “securities” or “futures contracts” and which are not, and this question remains a difficult one to answer.

The SFC Announcements stated that the SFC has developed a set of standard terms and conditions (the “T&Cs”)[3] to be imposed, by way of licensing conditions, on licensed corporations, in relation to:

1. their management of portfolios in which 10% or more of its gross asset value (GAV) are in virtual

assets (the “de minimis threshold”); and

2. their financial resources if they plan to hold non-SF Virtual Assets on behalf of portfolios under

their management.

In addition, all licensed corporations and license applicants are required to inform the SFC if it is presently managing or planning to manage (as the case may be) one or more portfolios that invest in virtual assets (regardless of whether the percentage of virtual assets in such portfolios is above or below the de minimis threshold) or if they intend to hold non-SF virtual assets on behalf of the portfolios under their management. This requirement, together with the requirement to comply with the T&Cs, are referred to as “Asset Manager Requirements”.

As noted above, SFC Announcements do not contain any new laws and as such do not re-define who may or may not require an SFC license. In other words, if a market participant was required to obtain a type of SFC license before the SFC Announcements, then it would be required to do so after the SFC Announcements and vice versa.

LICENSING OF VIRTUAL ASSET MANAGERS AND VIRTUAL ASSET FUNDS DISTRIBUTORS

Box 1

Those falling within Box 1 are required to comply with the Asset Manager Requirements. The SFC specifically noted the T&Cs do not apply to licensed corporations which only manage portfolios that invest in virtual asset funds (ie funds of virtual asset funds). This is an expected and sensible regulatory outcome. However, it is interesting to note the reason which the SFC gave for this – it is because the existing requirements, especially the Fund Manager Code of Conduct, are considered adequate for governing the management of funds of funds. The reason is not because (or at least not explicitly stated to be because) the fund manager managing virtual asset fund of funds is in fact managing a portfolio of funds (units of such funds being traditional securities), as opposed to managing a portfolio of the underlying virtual assets. The latter reasoning (ie the reason not stated) would have been far more robust and technically convincing.

Box 2

Those falling within Box 2 would be required to comply with the Asset Manager Requirements in the same manner as those falling within Box 1.

The consequences of the SFC Announcements on those market participants falling in Box 2 are perhaps most difficult to conceptually justify, and perhaps are the most significant departure from the SFC’s previous practice of regulating SFC licensed corporations. Effectively, the SFC has extended its regulatory reach by supervising unregulated activities of licensed corporations solely on the basis that such (unregulated) activities are conducted by an SFC licensed firm. However, the positive outcome of this extension of regulatory reach is that the SFC has tacitly approved the practice of managing a portfolio of non-SF Virtual Assets alongside a licensed corporation’s portfolio of traditional securities or futures contracts. Previously there has been some anecdotal evidence that the SFC may not have been too enthusiastic about this practice, although conducting unregulated activities as a business by an SFC licensed corporation in itself is nothing new.

Box 3

Those falling within Box 3 are required to obtain an SFC Type 9 license (as would have been the case before the SFC Announcements) and comply with the Asset Manager Requirements.

Box 4

Those falling within Box 4 are not required to get any SFC license. When compared to those falling within Box 2, it appears that there is an un-level playing field between those managing a portfolio of non-SF Virtual Assets with a Type 9 license (ie Box 2), and those managing a portfolio of non-SF Virtual Assets without a Type 9 license (ie Box 4) because those in Box 2 will be subject to SFC regulatory requirements whereas those in Box 4 can operate without a license at all and not be subject to any regulatory requirements. It appears that by taking this approach, the SFC is taking the view that it is better to regulate only part of the industry than to not regulate at all, even though regulating only part of the industry still leaves a regulatory gap and creates an un-level playing field for managers. For those who wish to manage a portfolio of non-SF Virtual Assets (and assuming they don’t intend to market in Hong Kong or to the Hong Kong public) and who don’t wish to be subject to the Asset Manager Requirements, the simple solution appears to be to manage such portfolio of non-SF Virtual Assets in a separate, unlicensed entity.

Box 5

Those falling within Box 5 will be subject to additional requirements (the “Additional Requirements”) as set out in the Circular (please refer to Part A, Part B and Part C of the Circular). These Additional Requirements would apply to those intermediaries who distribute virtual asset funds which are not authorised by the SFC and which have a stated investment objective to invest in virtual assets or intend to invest or have invested above the de minimis threshold in virtual assets directly or indirectly.

There are some uncertainties as to whether the Additional Requirements would apply to all SFC licensed corporations who distribute virtual asset funds or only apply to SFC licensed corporations who distribute such funds in Hong Kong or to the Hong Kong public and only with respect to people in Hong Kong or those who constitute the Hong Kong public (whether or not in Hong Kong to the extent that such Hong Kong public can exist outside of Hong Kong). However, the context in which the Circular was made was in relation to “any person who carries on a business in the distribution of interests in a collective investment scheme in Hong Kong or to the Hong Kong public”. On this basis, it appears one can reasonably assume that the Additional Requirements would not apply to licensed corporations with respect to their investors who are outside of Hong Kong or who are not Hong Kong public.

Box 6

Those falling within Box 6 are required to apply for an SFC Type 1 license (as would have been the case before the SFC Announcements) and need to comply with the Additional Requirements.

A common question is why a Type 1 license is needed even if the virtual assets held by the funds that are being distributed are considered to be non-SF Virtual Assets. Distributing a fund is a Type 1 regulated activity regardless of whether the assets held by the fund are “securities” and/or “futures contracts”. This is because Type 1 regulated activity is “dealing in securities” and the securities that are being dealt (ie that are being bought or sold) are the units of the funds that are being distributed, and not the assets held by the Fund. Hence it is irrelevant whether the assets held by the Fund are considered “securities” or “futures contracts”.

FRAMEWORK FOR REGULATING VIRTUAL ASSET TRADING PLATFORM OPERATORS

The SFC has adopted a different, wait-and see approach to regulating virtual asset trading platform operators (the “VA Operators”). Appendix 2 of the Statement provides a conceptual framework for the SFC to license and regulate VA Operators. The SFC intends to, in a sandbox environment, explore whether it is appropriate to grant a license to and regulate any of these VA Operators under its existing powers. VA Operators may approach the SFC if they are interested in being licensed and to demonstrate their commitment to adhering to the SFC’s requirements.

By adopting such an approach, the SFC has left open different possible regulatory outcomes for market participants and allowed itself possibilities of different regulatory approaches in the future. At this stage, in deciding whether to opt-in to the sandbox, VA Operators need to decide whether the credibility which may be brought with a licensed status would be worth the regulatory burden such a license status would entail.

CONCLUDING REMARKS

It is clear that investor protection is the top agenda in the SFC Announcements and, as is often the case, the SFC has largely relied on its usual twin arrow in its armory to target investor protection, namely enhanced disclosures for investors and suitability assessment. The former imposed on product providers/originators and the latter imposed on product distributors. However, difficulties remain for both regulators and market participants alike in a regulatory regime where the regulation of financial activities is fundamentally based on outdated definition and concepts of “securities” and “futures contracts”. These difficulties are made obvious when the existing definitions of “securities” and “futures contracts” are applied to a new asset class such as virtual assets.

=========================================

For further details on how we can assist you, please contact us at: [email protected].

This material is for general information only and is not intended to provide legal advice.

=========================================

Ben Wong

© ALTQUEST LIMITED

NOVEMBER 2018

[1]https://www.sfc.hk/web/EN/news-and-announcements/policy-statements-and-announcements/reg-framework-virtual-asset-portfolios-managers-fund-distributors-trading-platform-operators.html

[2]https://www.sfc.hk/edistributionWeb/gateway/EN/circular/doc?refNo=18EC77

[3]

See pages 2-6 of https://www.sfc.hk/web/EN/files/ER/PDF/App%201%20-%20Reg%20standards%20for%20VA%20portfolio%20mgrs_eng.pdf